Dr Kristian Niemietz is the IEA’s Editorial Director and Head of Political Economy

Suppose I claimed that the band Coldplay peaked around the year 2000, in terms of their commercial success, and has been declining ever since. Suppose I was basing this assessment on their sales of CDs.

You would immediately see the flaw in that argument. For comparisons over time, CD sales are a terrible measure of success or failure – at least for this period. The turn of the millennium was the peak of the CD era. Since then, CD sales have been declining worldwide, first slowly, then rapidly. Today, the CD has gone almost extinct, as a medium. I bet some of my Zoomer colleagues have never even seen one.

So if I told you that a band sold 100,000 CDs in a particular year, that doesn’t mean much, on its own. You won’t know whether that’s good or bad, unless I provide additional context. In 2000, a sales figure like that would have been considered a flop. Ten years ago, it would have been a major success. Today, it would be almost a miracle.

Something similar is true for comparisons of economic growth rates between different periods. If a Western economy grows by 1 per cent per year over a certain period, is that good or bad? The answer depends on what period we are talking about.

If an economy managed to grow at that rate during the Great Depression, the Great Financial Crisis or during Covid, that’s great. But if that’s during an international boom, it’s not. For example, there was once a 32-year period during which the Swiss economy used to grow by just under half a percent per annum, which does not sound like a lot. But nobody considers it an economic policy failure. Because that period was 1913 to 1945.

I know what you’re thinking: “Impressive stuff, Niemietz. Next, you’re going to tell us that a temperature that’s considered warm in January would not be considered warm in July. How did you not get the Nobel Prize in economics yet?” And yet – I have seen people engage in the economics equivalent of the ‘CD Sales Fallacy’. I have seen people compare Britain’s postwar growth rates directly to those of the 1980s and 1990s, and conclude that the postwar model was superior to ‘neoliberalism’.

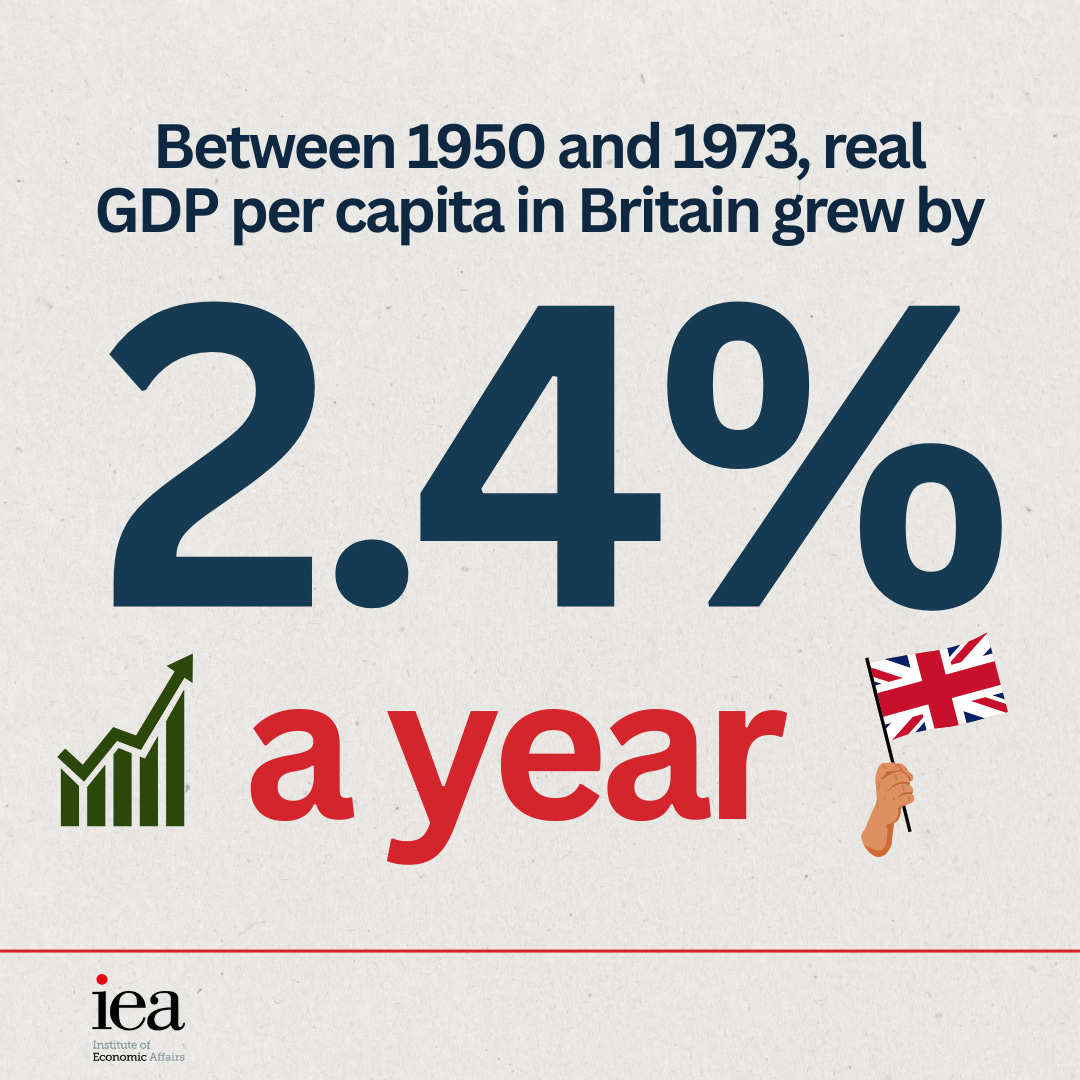

It is true that, compared to other periods, Britain’s postwar economic performance looks solid. Between 1950 and 1973, real GDP per capita used to grow by 2.4 per cent a year, and real GDP per working hour by almost 2.9 per cent. If a present-day British government oversaw such growth rates, we almost certainly wouldn’t be burning through Prime Ministers at an Italian rate, and our more durable Prime Minister would never stop bragging about those figures.

But postwar Britain was nonetheless not an economic success story. Virtually everyone else was growing at rates above 4 per cent at the time. France and Italy managed just over 5 per cent, West Germany and Austria around 6 per cent. Britain started the postwar era with a massive lead over most other Western economies, and squandered that lead over the subsequent twenty-odd years.

While the postwar period is remembered very fondly in British folk memory, the same is true everywhere else as well. The French call that period les Trente Glorieuses, the (West) Germans and the Austrians call it the Wirtschaftswunder, the Italians il Miracolo Economico, and with differences in timing, Spain has its own version, el Milagro Español.

What was so special about that period? It seems rather unlikely that every government in the Western world suddenly started to make terrifically good economic policy choices at the same time. We can also discount policy-based explanations on the grounds that economic policies differed a lot from place to place: there is no common ‘postwar model’. So what is it that makes that era special?

I won’t pretend to be an expert on this. But my semi-informed understanding is that the cataclysmic events of 1914–1945 created a ‘modernisation dam’: technological and organisational innovations were still happening, but their diffusion was slowed down or blocked. Then after 1945, the dam burst, and a lot of the economic modernisations that might otherwise have been widely adopted in the first half of the 20th century washed all over the West’s economies all at once. I have seen economic historians argue that this thesis has its gaps, and that it cannot be the whole story, but I have not seen anyone argue that it is wrong.

Now, when it comes to prosperity, I’m generally more interested in the absolute than in the relative picture. If the living standard of the average Brit improves – that’s good. If the living standards of other people improve at an even faster rate – even better for them. Economic league tables are not football league tables; the economic success of one country does not diminish the economic success of another.

But relative figures matter insofar as they give us an idea of what was possible at a particular time, and postwar Britain fell far short of what was possible. It was therefore not a success story. It was a period when overripe low-hanging fruits were dropping into people’s mouths.

There’s nothing wrong with nostalgia. It doesn’t matter if people remember a summer as sunnier, or a Christmas as whiter, than it truly was. My problem with postwar nostalgia is that people draw the wrong conclusions from it. The fashionable interpretation is that the postwar years were a good time, because Britain was getting a break from economic liberalism. But the association of the postwar period with economic statism is a specifically British perspective.

There have been attempts to project economic freedom scores back in time, and judging from those, it is not the case that the 1950s, 1960s and 1970s were generally a less liberal period than the 1880s, 1890s and 1900s. They were in Britain, yes. But they were clearly not in West Germany, Austria, Japan or the United States.

Did Britain grow more strongly during the relatively liberal 1990s than during the relatively illiberal 1950s? No. It did not. But within any given period, it is the more liberal economies that tend to outperform that less liberal ones. That is the relevant comparison.

You can get away with nationalisations, price controls, excessive money-printing and Mazzucatoism, but only if you have a reservoir of pent-up innovations ready to be unleashed on the economy, as Britain did in 1945. We don’t have that today, and we better act accordingly.

| A guest post by

|